Fixed overhead variances

kevc90

Registered Posts: 8

Hello,

Wonder if someone could help me with the expenditure variance for the below:

Budgeted production is 10,000 units @ 6 hours per unit with a labour cost of 5 pounds per hour

Actual production is 11,500 units using 70,150 hours at a total cost of 343,735

Overheads are apportioned on the basis of budgeted total labour hours. Total fixed overheads are budgeted at 600,000 with actuals of 630,000

Any general tips on understand these would be appreciated!!

Wonder if someone could help me with the expenditure variance for the below:

Budgeted production is 10,000 units @ 6 hours per unit with a labour cost of 5 pounds per hour

Actual production is 11,500 units using 70,150 hours at a total cost of 343,735

Overheads are apportioned on the basis of budgeted total labour hours. Total fixed overheads are budgeted at 600,000 with actuals of 630,000

Any general tips on understand these would be appreciated!!

0

Comments

-

BPP have recently published amendments to MDCL.

https://s3-eu-west-1.amazonaws.com/bppassets/public/assets/pdf/learning-media/Update-to-the-MDCL-Assessment.pdf0 -

Hi,

Just incase you haven't gotten the answer to your Q.

Fixed Overhead Expenditure : Actual - Budget

£630,000 - £600,000 = £30,000

Fixed Overhead Volume : Budget - SH * SR (Standard Hour * Standard Rate)

£600,000 - 300,000 (10,000*6*5) = 300,000

Fixed Overhead Capacity : Budget - AH * SR (Actual Hour * Standard Rate)

£600,000 - 350750 (70150*5) = 249250

Fixed Overhead Efficiency: AH * SR - SH * SR (Standard Hour * Standard Rate)

350750 - 300,000 = 50,750

Total Fixed Overhead : Actual - SH * SR (Standard Hour * Standard Rate)

£630,000 - 300,000 = 330,0001 -

0 -

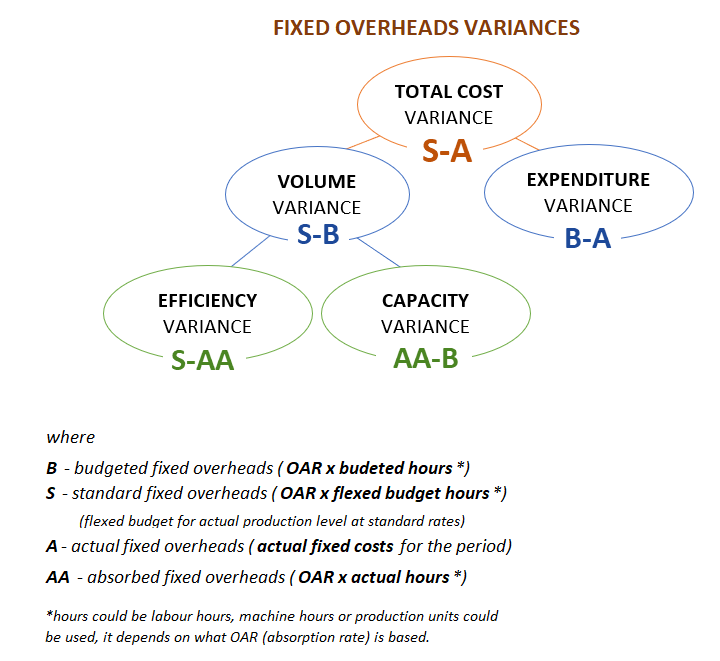

OAR = 600,000/60,000 = £10/labour hour

B= £600,000

S=£10 x (11500 x 6 h) = £690,000

A=£630,000

AA=£10 x 70,150= £701,500

Fixed overhead expenditure: B-A = 600,000 - 630,000= -30,000 (Adverse)

Volume variance: S-B=690,000-600,000= 90,000 (Favourable)

Capacity variance: AA-B = 701,500 -600,000 = 101,500 (Favourable)

Efficiency variance: S-AA = 690,000 - 701,500 = -11,500 (Adverse)0

Categories

- All Categories

- 1.3K Books to buy and sell

- 2.3K General discussion

- 12.5K For AAT students

- 390 NEW! Qualifications 2022

- 174 General Qualifications 2022 discussion

- 16 AAT Level 2 Certificate in Accounting

- 78 AAT Level 3 Diploma in Accounting

- 114 AAT Level 4 Diploma in Professional Accounting

- 8.9K For accounting professionals

- 23 coronavirus (Covid-19)

- 276 VAT

- 96 Software

- 281 Tax

- 148 Bookkeeping

- 7.2K General accounting discussion

- 211 AAT member discussion

- 3.8K For everyone

- 38 AAT news and announcements

- 345 Feedback for AAT

- 2.8K Chat and off-topic discussion

- 589 Job postings

- 16 Who can benefit from AAT?

- 37 Where can AAT take me?

- 43 Getting started with AAT

- 26 Finding an AAT training provider

- 48 Distance learning and other ways to study AAT

- 24 Apprenticeships

- 67 AAT membership