Fixed overhead variances (easy)

Anzelari

Registered Posts: 11 New contributor 🐸

Hi everyone,

Hope the following will help you calculate fixed overhead variance very quickly.

After 2 days of trying to remember all the formula used to calculate the variances. I remembered what our professor was saying in the university: "Mathematics do not have to remember they have to get it using the logic".

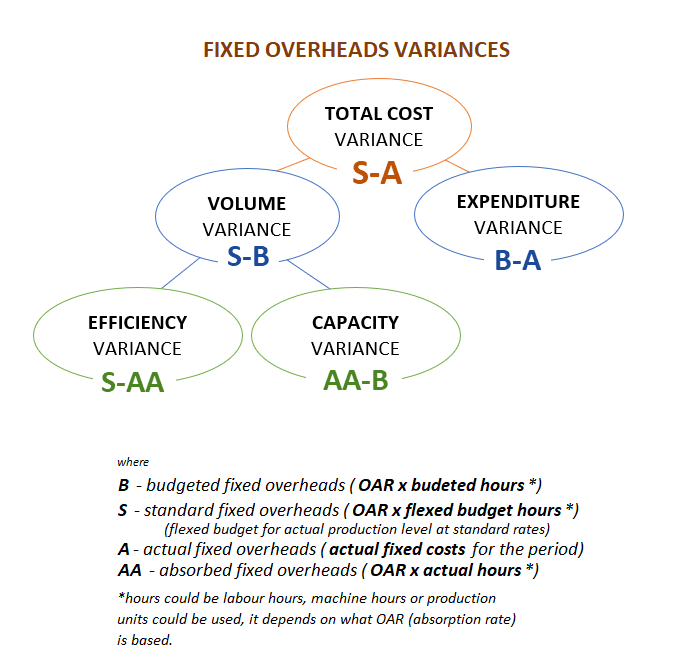

And I found the logic in fixed overhead calculations. Just remember easy formulas S-A = (S-B) + (B-A) and S-B = (S-AA) + (AA-B), where

B - Budgeted overheads, S - Standard overheads, A- Actual overheads, AA- Absorbed overheads

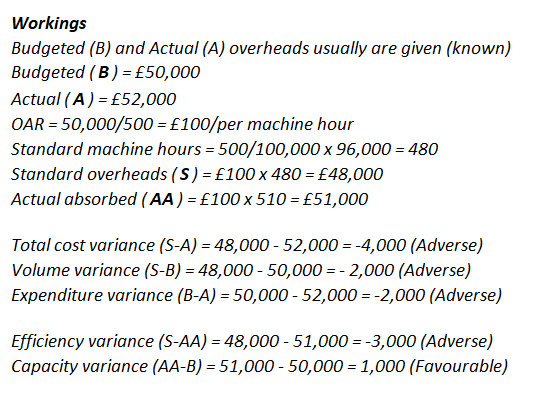

B and A are usually known, Standard overheads = OAR x standard hours (calculated using flexing budget rules), AA = actual hours x OAR

please, see the picture for more information

Hope the following will help you calculate fixed overhead variance very quickly.

After 2 days of trying to remember all the formula used to calculate the variances. I remembered what our professor was saying in the university: "Mathematics do not have to remember they have to get it using the logic".

And I found the logic in fixed overhead calculations. Just remember easy formulas S-A = (S-B) + (B-A) and S-B = (S-AA) + (AA-B), where

B - Budgeted overheads, S - Standard overheads, A- Actual overheads, AA- Absorbed overheads

B and A are usually known, Standard overheads = OAR x standard hours (calculated using flexing budget rules), AA = actual hours x OAR

please, see the picture for more information

1

Comments

-

1 -

0 -

0 -

That's one way . . .

I prefer - Total OH Variance is the difference between what it did cost and what it should have cost.

This total variance breaks down into expenditure variance (which ignores the 'should have' bit) and volume variance.

Volume then breaks down again into efficiency and capacity.

Capacity Variance is the one that usually causes problems as it is not so instinctive. If we actually use fewer hours than the original base budget, this is Adverse because we ae not fully using those assets we have invested in.0 -

Hi, mcchoc. Thank you for your comment! How do you remember how to calculate all these variances?

0 -

As mcchoc says, look at the difference between what should happen and what actually happened.

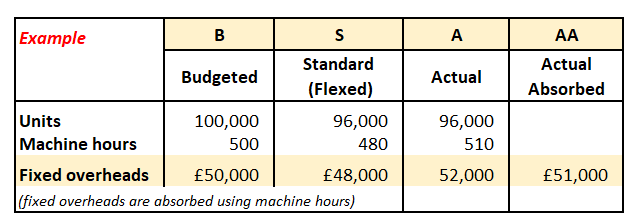

In your example, each unit should take 0.005 hours (500/100,000) and you recover £100 overhead per hour (£50,000/500)

So, 96,000 units should take 480 hours (96,000 x 0.005)

They actually took 510 hours, 30 hours too long

This is an efficiency problem, which reduces your overhead recovery by £3,000 (30 hrs x £100/hr)0 -

Foolproof method for Materials and Labour variances

Create three columns BudgetActualStandard

Under each title, tear the data to shreds, ie kg/unit, £/kg, total Kg, total material cost; hours/unit, £/labour hour, total labour hours, total labour cost.

Remember - the Standard Budget is just the original budget flexed by the new Volume, so we flex the quantities of materials and labour hours, but NOT the unit price.

0

Categories

- All Categories

- 1.3K Books to buy and sell

- 2.3K General discussion

- 12.5K For AAT students

- 388 NEW! Qualifications 2022

- 171 General Qualifications 2022 discussion

- 16 AAT Level 2 Certificate in Accounting

- 78 AAT Level 3 Diploma in Accounting

- 115 AAT Level 4 Diploma in Professional Accounting

- 8.9K For accounting professionals

- 23 coronavirus (Covid-19)

- 276 VAT

- 96 Software

- 281 Tax

- 147 Bookkeeping

- 7.2K General accounting discussion

- 211 AAT member discussion

- 3.8K For everyone

- 38 AAT news and announcements

- 345 Feedback for AAT

- 2.8K Chat and off-topic discussion

- 589 Job postings

- 16 Who can benefit from AAT?

- 37 Where can AAT take me?

- 42 Getting started with AAT

- 26 Finding an AAT training provider

- 48 Distance learning and other ways to study AAT

- 24 Apprenticeships

- 67 AAT membership