Management Accounting: Costing (AQ2016)- Practice Assessment 1 - 1.7

Ssanta

Registered Posts: 6 New contributor 🐸

1.7

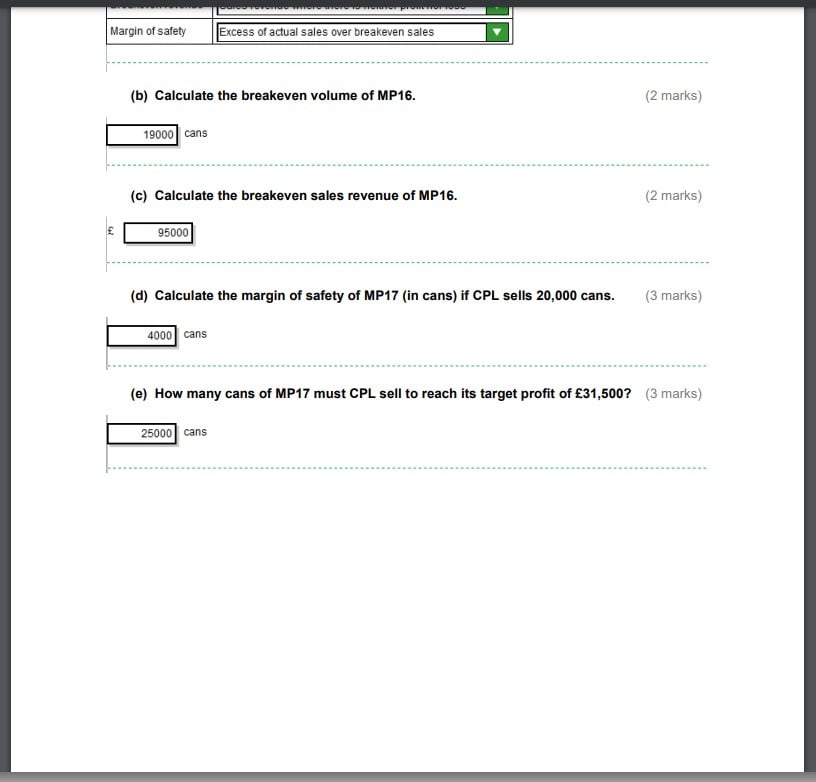

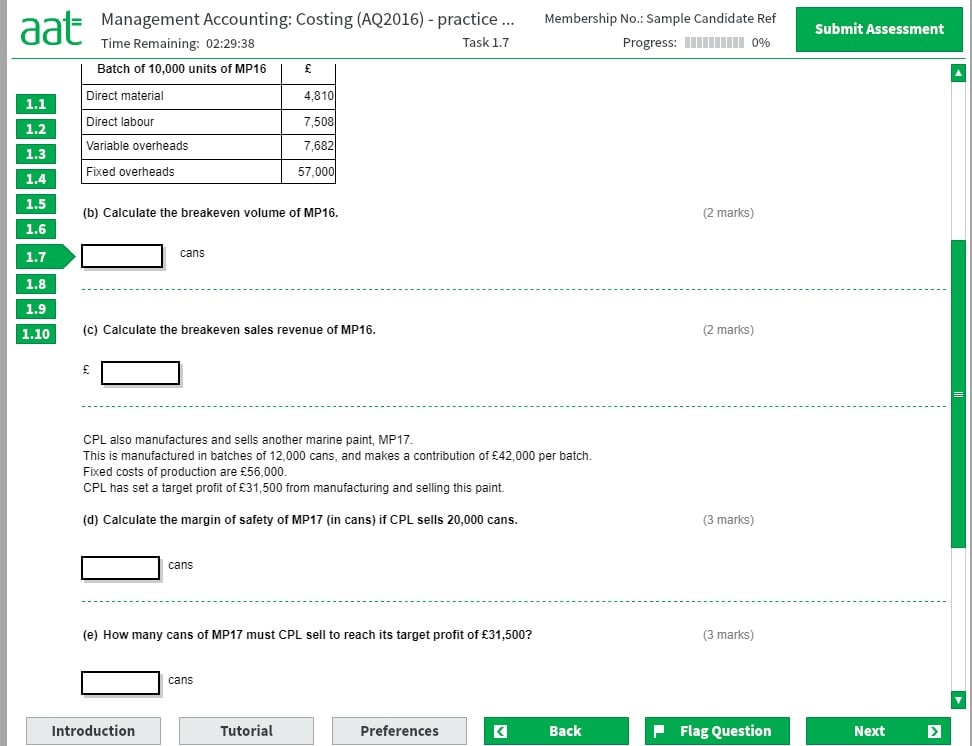

b) Breakeven volume = fixed costs / contribution per unit

(fixed costs)57000/(contribution per unit) ?

? = contribution is sales revenue less the variable costs

(sales revenue) 50000 (10000 cans £5.00 each) "less" - (contribution per unit) 20000 (Direct mat. 4810+ Direct labour 7508 + variable overheads 7682)=50000-20000=30000

Contribution per unit = 57000/30000=1.9 (can)

Break even Volume = 1.9*10000=19000 (per volume)

c) Breakeven Sales Revenue = 19,000 cans x selling price (£5.00) = Total revenue £95,000

d)Margin of safety (20000 cans)

Margin of safety = Budgeted sales units - brake even, = 20000- ?

? = brake even = fixed costs/ contribution per unit (42000 (contribution)/12000 (units))= 56000/3.5=16000

Margin of safety = 20000-16000=4000 units

e) how many cans to sell to reach its target profit

=(fixed costs + target profit)/contribution per unit

= (56000+31500)/3.5

=87500/3.5

=25000 cans

b) Breakeven volume = fixed costs / contribution per unit

(fixed costs)57000/(contribution per unit) ?

? = contribution is sales revenue less the variable costs

(sales revenue) 50000 (10000 cans £5.00 each) "less" - (contribution per unit) 20000 (Direct mat. 4810+ Direct labour 7508 + variable overheads 7682)=50000-20000=30000

Contribution per unit = 57000/30000=1.9 (can)

Break even Volume = 1.9*10000=19000 (per volume)

c) Breakeven Sales Revenue = 19,000 cans x selling price (£5.00) = Total revenue £95,000

d)Margin of safety (20000 cans)

Margin of safety = Budgeted sales units - brake even, = 20000- ?

? = brake even = fixed costs/ contribution per unit (42000 (contribution)/12000 (units))= 56000/3.5=16000

Margin of safety = 20000-16000=4000 units

e) how many cans to sell to reach its target profit

=(fixed costs + target profit)/contribution per unit

= (56000+31500)/3.5

=87500/3.5

=25000 cans

0

Categories

- All Categories

- 1.3K Books to buy and sell

- 2.3K General discussion

- 12.5K For AAT students

- 390 NEW! Qualifications 2022

- 174 General Qualifications 2022 discussion

- 16 AAT Level 2 Certificate in Accounting

- 78 AAT Level 3 Diploma in Accounting

- 114 AAT Level 4 Diploma in Professional Accounting

- 8.9K For accounting professionals

- 23 coronavirus (Covid-19)

- 276 VAT

- 96 Software

- 281 Tax

- 148 Bookkeeping

- 7.2K General accounting discussion

- 211 AAT member discussion

- 3.8K For everyone

- 38 AAT news and announcements

- 345 Feedback for AAT

- 2.8K Chat and off-topic discussion

- 589 Job postings

- 16 Who can benefit from AAT?

- 37 Where can AAT take me?

- 43 Getting started with AAT

- 26 Finding an AAT training provider

- 48 Distance learning and other ways to study AAT

- 24 Apprenticeships

- 67 AAT membership