Chargeable Gain/loss On House Disposal

clarisse

Registered Posts: 8 New contributor 🐸

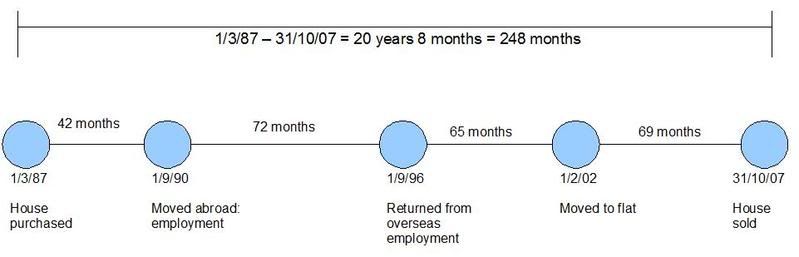

Bought house 1/3/87 £36000

Lived in house until 1/9/90 then went o/seas to take up employment.

Returned from there on 1/9/96 , moved back into house until 1/2/02 when new flat purchased.

He lived in flat since then.

Sold house for £178000 on 31/10/07.

Have major problems identifying the months covered ie occupied , deemed occuped & absent.

Please can someone explain this in laymans terms how to identify the months relating to the stay in each of the above headings.

Really need to grasp this asap as the exam is next month.

many thanks

Clarisse

Lived in house until 1/9/90 then went o/seas to take up employment.

Returned from there on 1/9/96 , moved back into house until 1/2/02 when new flat purchased.

He lived in flat since then.

Sold house for £178000 on 31/10/07.

Have major problems identifying the months covered ie occupied , deemed occuped & absent.

Please can someone explain this in laymans terms how to identify the months relating to the stay in each of the above headings.

Really need to grasp this asap as the exam is next month.

many thanks

Clarisse

0

Comments

-

First place I would start when answering this question is to put a timeline of the events. I would put this in my answer as it shows how you have come to the length of periods you will use later.

Now, before we come to answer the question, lets remind ourselves of the "deemed occupation" rules.

Firstly, the final 36 months of ownership is deemed occupation as long as the house was the owners PPR at any given time during the ownership. Unlike the other rules, he does not need to come back to the house afterwards.

To claim residence for other periods of absence,

"both before and after the period of absence there must be a time during which the dwelling house is the individual's only or main residence." (HMRC definition), and

no other property is being treated as PPR during period of absence.

Provided this is the case, the owner can claim:

- a period of absence of any length throughout which they worked in an employment outside the United Kingdom,

- a maximum of four years during which they could not live in the house because of Employment within the United Kingdom, and

- periods of absence, for any purpose, which do not exceed three years in total.

Also remember that absence can be claimed for a combination of reasons, e.g. if there was a period they were absent due to UK employment of 5 years, they can claim 4 years because of the UK employment rule, and the other year can be claimed as part of their 3 years for any reason.

Now, back to the question.

Underneath the timeline, I would then set out the periods and explain whether they are occupied, deemed occupied/exempt from charge (and why), or absent.

1/3/87-31/8/90= 3 years and 6 months(42 months) Lived in house, therefore exempt.

1/9/90-31/8/96 = 6 years(72 months). Went to Australia for employment, which is exempt period of absence due to employment outside the United Kingdom.

1/9/96-31/1/02 = 5 years and 5 months (65 months). Lived in house, therefore exempt.

1/2/02-31/10/06 = 5 years and 9 months (69 months). Left house(moved to small flat). Last 36 months (1/11/04-31/10/07) are exempt as per HMRC rules as house was occupied by owner previously. Balance of 33 months (69 - 36) is chargeable.

Now we calculate the gain:

Proceedsless: Cost178,000less: Indexation*(36,000)Gain for whole period before Taper(22,187)119,813

* Indexation for March 1987 to April 1998: [(162.6-100.6)/100.6] x 36,000= £22,187 (to nearest pound)

Then we calculate the chargeable gain by multiplying the gain by:

Period not occupied

Period owned

Chargeable gain: £119,813 x (33/248) = £15,942 (Gains are rounded down)

The gain of £15,492 would then be 60% chargeable based on 9+1 years; 9 complete years between April 1998 and October 2007, plus a bonus year for ownership before 17/3/980 -

Chargeable gain/loss

Hi Mehmet, sorry for the delay in reply to your e-mail 19/11.

Thank you for your help on the PRR , the penny eventually dropped after.

It's a pity it didn't appear in the exam last week.

Hopefully i've done enough on the DFS & PTC , lets see what happens in Feb

regards

C0

Categories

- All Categories

- 1.3K Books to buy and sell

- 2.3K General discussion

- 12.5K For AAT students

- 390 NEW! Qualifications 2022

- 174 General Qualifications 2022 discussion

- 16 AAT Level 2 Certificate in Accounting

- 78 AAT Level 3 Diploma in Accounting

- 114 AAT Level 4 Diploma in Professional Accounting

- 8.9K For accounting professionals

- 23 coronavirus (Covid-19)

- 276 VAT

- 96 Software

- 281 Tax

- 148 Bookkeeping

- 7.2K General accounting discussion

- 211 AAT member discussion

- 3.8K For everyone

- 38 AAT news and announcements

- 345 Feedback for AAT

- 2.8K Chat and off-topic discussion

- 589 Job postings

- 16 Who can benefit from AAT?

- 37 Where can AAT take me?

- 43 Getting started with AAT

- 26 Finding an AAT training provider

- 48 Distance learning and other ways to study AAT

- 24 Apprenticeships

- 67 AAT membership